For Americans already struggling with the highest mortgage rates in a generation, new legislation out of Washington promises little relief. The “One Big Beautiful Bill Act” (OBBBA) will add trillions to the national debt over the next decades, further cementing an era of expensive borrowing.

The basic laws of supply and demand suggest this surge in government debt issuance will push interest rates even higher for everyone, straining the already-frozen housing market and increasing costs for all types of credit.

The one silver lining, though, is that the sooner lenders accept our “higher for longer” new world of interest rates, the sooner they can stop worrying so much about prepayment risk, which may shrink the spread they charge above 10-year Treasury yields. Below, we’ll explore how national debt impacts real estate.

As Uncle Sam borrows ever more, everyone’s interest rates will rise

The One Big Beautiful Bill Act, enacted this summer, puts the pedal to the metal for debt accumulation over the next decade in the U.S. The Committee for a Responsible Federal Budget estimates that it will add a cumulative $5.5 trillion to the debt by 2034, under the realistic assumption that its provisions written to expire will instead be extended, as has become normal in federal budgeting.

Even taking the expirations at face value, though, the bill raises deficits by a cumulative $4.1 trillion, an extraordinary choice in the midst of an economic expansion and coming on the heels of the worst bout of inflation in decades.

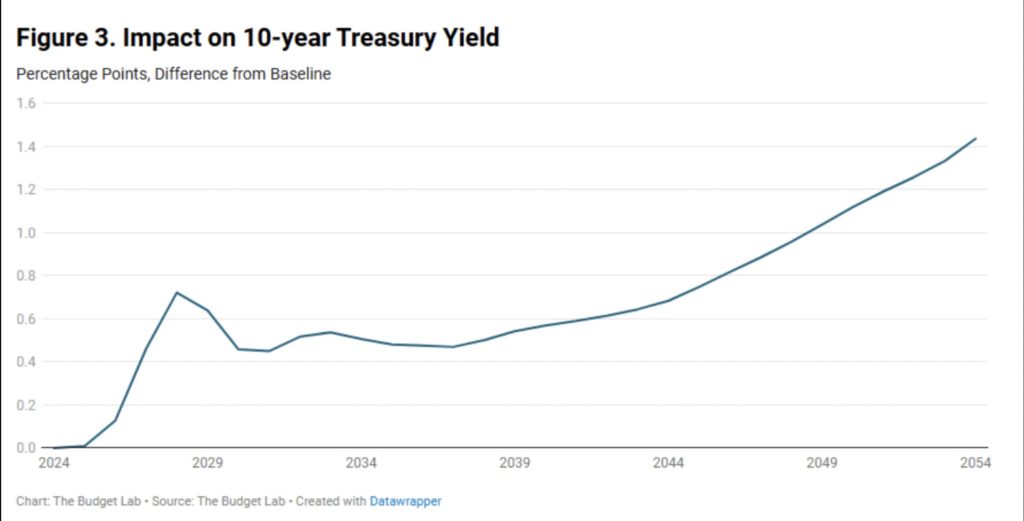

The issuance of trillions of dollars of additional debt in the next several years is expected to drive up interest rates. The Budget Lab at Yale has estimated that the bill will raise 10-year Treasury yields by about half a point in the next several years and by more than 1.4 points in the very long run.

This is driven in part by their modeling assumption that the Federal Reserve will succeed at keeping inflation close to 2 percent, which will require higher interest rates in the long run. They also expect a higher term premium on long-term debt, like 10-year Treasuries.

Altogether, this paints a picture of government borrowing crowding out private borrowing — as the Treasury issues more debt to finance its deficits, yields must rise to compensate investors. Other debt in the economy, such as mortgages, must yield more as well, in order to compete with Treasury bonds for lenders.

High interest rates have already frozen the housing market

While the U.S. economy continues to grow, the U.S. housing market has been stuck in neutral for over three years. Ever since mortgage interest rates rebounded from all-time lows below 3 percent for 30-year loans in 2020 and 2021, to generational highs above 7 percent in 2023, existing-home sales have been stuck in the neighborhood of 4 million annual sales.

It’s no surprise that fewer homes are changing hands than during the 2021 low-interest-rate boom, but 4 million is much fewer than even prevailed during the 2010s. In fact, 2024’s total of 4.06 million existing-home sales was the lowest total since the 1990s. The housing market is caught in a perfect storm, keeping homeowners frozen in place, thanks to the one-two punch of high price-to-income ratios and high mortgage rates.

While the OBBBA includes some sweeteners for certain homeowners, like the expansion of the state and local tax deduction cap to $40,000, the main long-term effect it promises for housing is just higher interest rates.

One near-term trend likely to help mortgage borrowers: a thinner spread

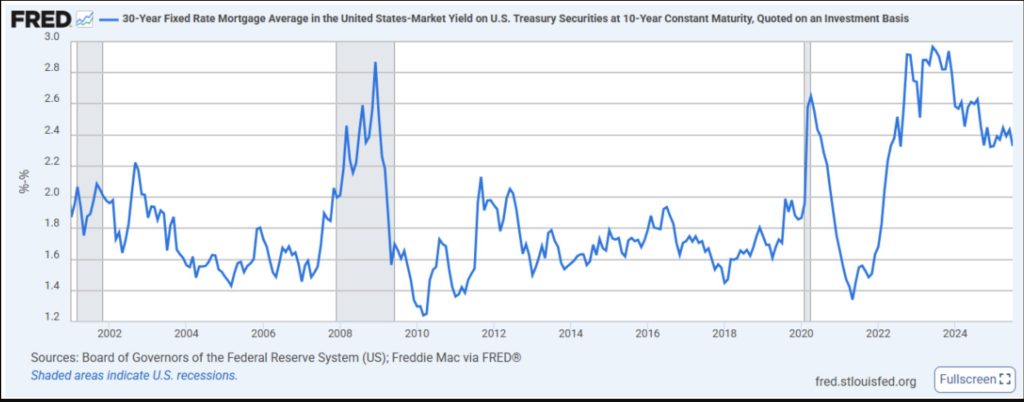

Bigger deficits, bigger debt, higher interest rates — the long-term fiscal outlook is getting darker. But there’s one silver lining that has begun to shine around the edge of these gathering clouds. The mortgage-Treasuries spread has begun to narrow again, resuming its progress back down toward pre-pandemic levels. The spread, here, refers to how much higher 30-year mortgage rates are averaging than 10-year Treasury yields.

In the 21st century, up to the pandemic, mortgage rates rarely exceeded 10-year Treasury yields by more than 2 percentage points, except during the global financial crisis. When mortgage rates soared back up in 2022, part of their climb was due to the widening spread. The two major reasons for widening spreads are a greater prepayment or refi risk on mortgages and interest rate volatility.

The latter has gradually faded this summer after spiking amidst tariff uncertainty in April. But the prepayment risk component is the bigger factor. For lenders and the investors who buy mortgage-backed securities, mortgages issued at high interest rates are uniquely risky because borrowers are expected to refinance them once mortgage rates fall back down.

The lack of a prepayment penalty for borrowers makes U.S. mortgages uniquely favorable to homebuyers here. If rates rise, they win by virtue of having locked in a lower rate; if rates fall, they can always refinance. Investors and lenders, by the same token, view refinancing as a unique downside to holding mortgages. They want a reliable coupon stream from mortgage holders’ monthly payments.

Seeing their loans wiped out by refinancing, replaced by cash in a new lower-interest-rate world, is a risk for which they must be compensated to make the loan in the first place.

That extra compensation for prepayment risk helped explain why mortgage rates soared even more than 10-year Treasury yields in 2022 and 2023. Now, though, as the reality sets in that we are living in a world where interest rates are “higher for longer,” lenders have gradually brought mortgage rates down relative to Treasuries, from about a 2.9-point spread in 2023 to 2.4 in recent months, or about one-third of the way back to normal.

The sooner investors conclude that refinancing prepayment risks aren’t so high, the sooner the spread can come down. The potential bankshot silver lining of the OBBBA? By putting a nail in the coffin of hopes for low interest rates, it may help further shrink the spread, so that higher 10-year Treasury yields don’t have to mean higher mortgage rates one-for-one.

Ultimately, the nation’s fiscal path points toward a new normal of higher borrowing costs for all. The “One Big Beautiful Bill Act” serves as an accelerant, solidifying a “higher for longer” interest rate environment that will impact everything from car loans to corporate debt. For the beleaguered housing market, this presents a bittersweet trade-off.

The bad news is that the foundational interest rate, the 10-year Treasury yield, is set to climb. The paradoxical good news is that by killing the hope of a return to ultra-low rates, the OBBBA may continue to shrink the risk premium lenders charge on mortgages. This narrowing spread won’t turn 7 percent mortgages back into 3 percent loans, but it might help us work our way back down closer to 6 percent.

Jeff Tucker is the Principal Economist at Windermere Real Estate in Seattle, WA. This blog was originally published on Inman News on 8/26/25.